By David R. Guttery, RFC, RFS, CAM

President, Keystone Financial Group-Trussville Al

Let me clearly preface that I’m not attempting to call a bottom here. No one can do that, and over the summer, some well-known business media personalities tried to do just that and weren’t successful. We won’t be able to accurately identify a bottom until we can see it in the rear-view mirror. I am encouraged by what, in my opinion seems to be, evidence that markets are finally doing what they normally do. They might be looking forward to the next 30 months instead of being fixated on the next 30 minutes, while the prospect of future conditions is priced into current assumptions.

There are also some quantifiable metrics that are present today, that we didn’t have in July when markets seemingly rallied over the summer. So, I’ll expound upon these during the video, but for now, at a high level, yes, I am optimistic that markets may indeed be coalescing around a near term bottom.

December will bring the 32nd anniversary of my being in practice. I’ve seen a lot over three decades. While participating in a WebEx on this topic recently, the thought occurred to me that I couldn’t recall a time over the course of my career anyway, when the Federal Reserve had seemingly been this restrictive and hawkish.

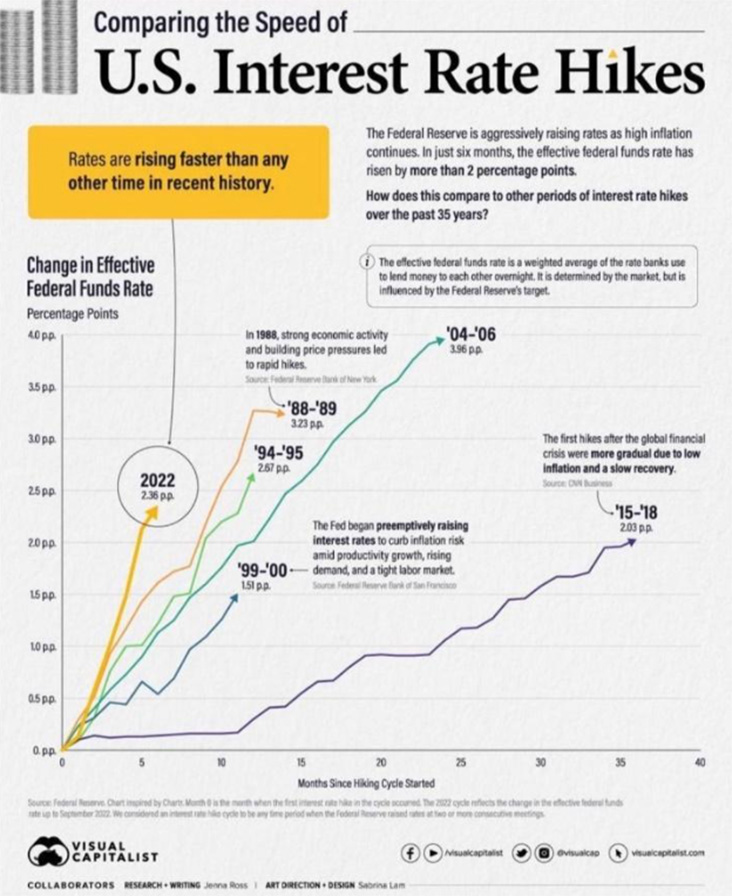

Ironically, I stumbled across this graphic shortly after the WebEx and it seems to confirm my suspicions. This illustrates major cycles of tightening over the last 35 years, and sure enough, the Federal Reserve is indeed more restrictive now, and being so much more rapidly, than at any other point over the last 35 years.

Ironically, I stumbled across this graphic shortly after the WebEx and it seems to confirm my suspicions. This illustrates major cycles of tightening over the last 35 years, and sure enough, the Federal Reserve is indeed more restrictive now, and being so much more rapidly, than at any other point over the last 35 years.

I believe that markets have priced into themselves, the assumption however that the Federal Reserve will remain blindly on a path to 450 basis points however, and that this posture of tightening will not relent. I’m not in that camp. We’ll find out in a few weeks when meeting minutes are released, but I believe that the Federal Reserve may find itself with the latitude to pursue targets of tightening, but with a less hawkish tenor, given the degree by which we can now measure economic deceleration.

Let me dispel a myth at this point. In my opinion, the Fed is not trying to control inflation. They are trying to disincentivize lending and borrowing. If they are successful, then the velocity of money should continue to decline, and hopefully leave us with fewer dollars chasing as many goods.

The Fed wants to stop short of disincentivizing production though, because it will defeat the purpose to have fewer dollars, chasing fewer goods. For this reason, I believe that the Fed may find the latitude to be less hawkish, and to potentially pursue tightening at a slower rate, and if they do, I believe the market will respond positively to this development.

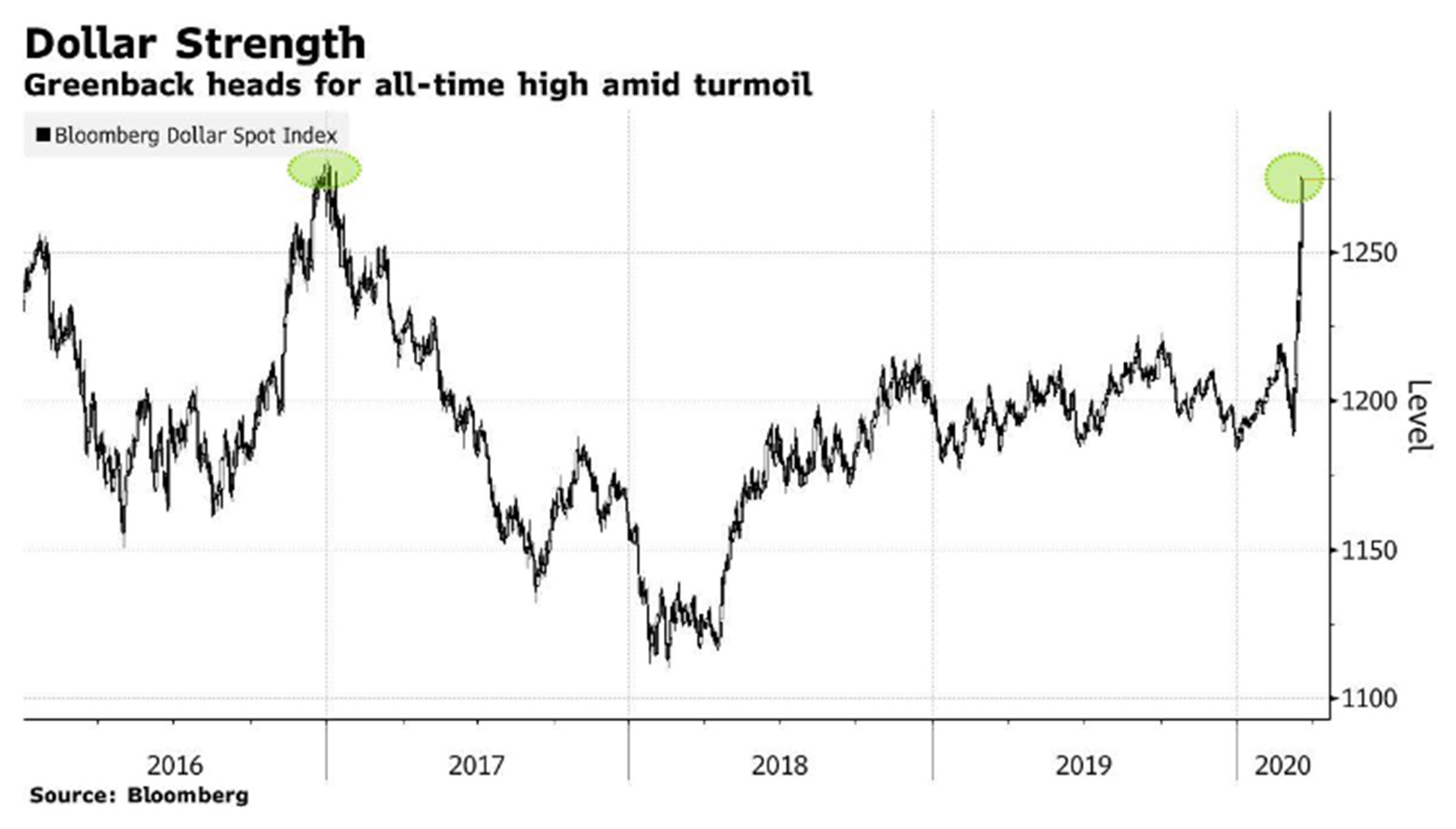

This is important because the actions taken by the Federal Reserve this year have strengthened the dollar to new highs against the global basket of currencies.

This is important because the actions taken by the Federal Reserve this year have strengthened the dollar to new highs against the global basket of currencies.

This is a key area of risk that markets have repriced all year. As goods are purchased with weaker foreign currencies, and those currencies repatriate as dollars, revenues are lower as a result.

Markets are repricing the risk that revenue estimates given twelve months ago, prior to record strength in the dollar, may not come to fruition. Should the Fed signal an intent to be less hawkish, this may indeed cause the dollar to weaken against the global basket of currencies, and thus be a positive for equities at this point.

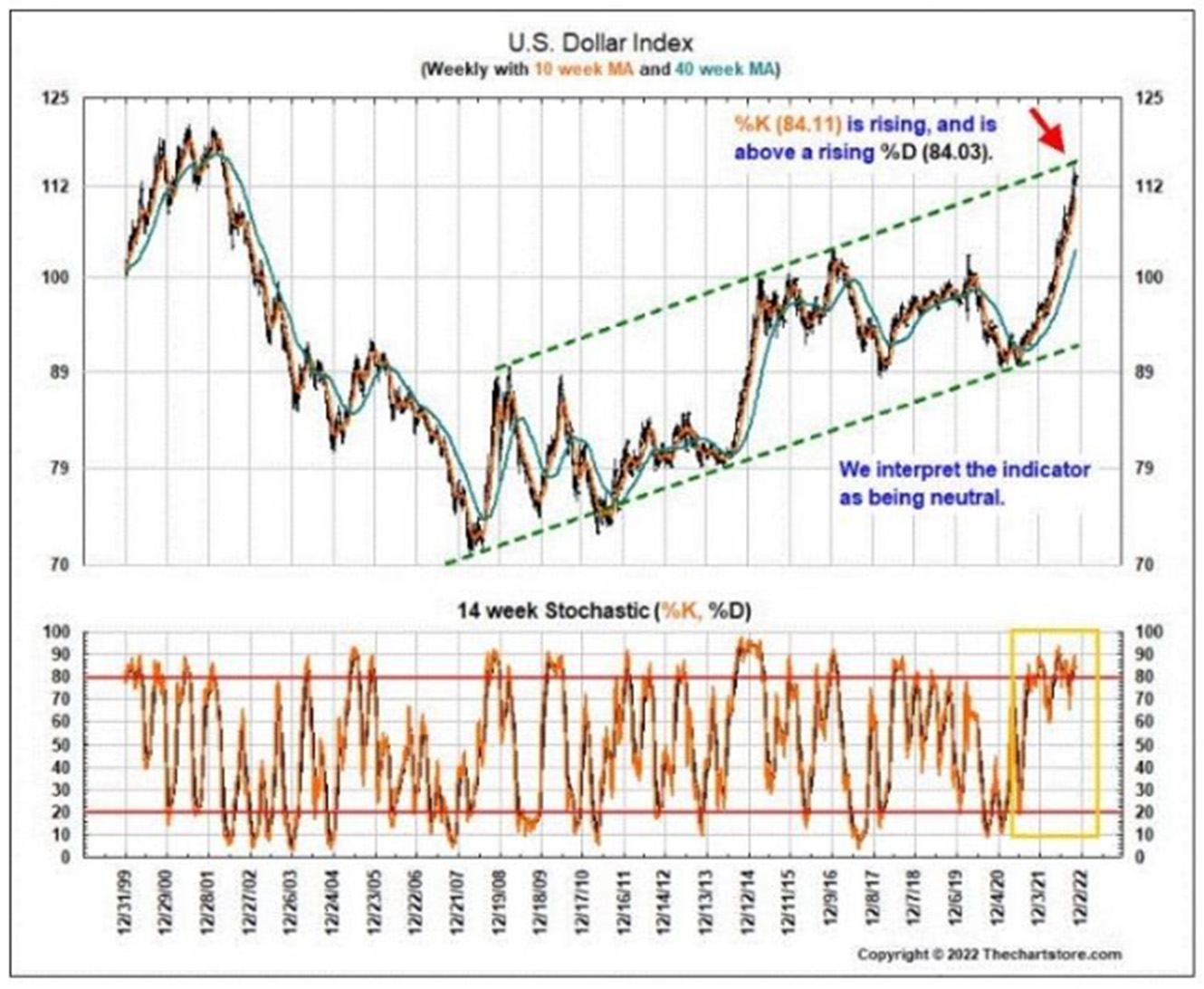

This chart seems to suggest that the recent strength in the dollar against the global basket may be running into resistance at these levels, and again, if this proves to be the case, it may be one of many catalysts around which the market can coalesce, and from which a bottom could precipitate.

This chart seems to suggest that the recent strength in the dollar against the global basket may be running into resistance at these levels, and again, if this proves to be the case, it may be one of many catalysts around which the market can coalesce, and from which a bottom could precipitate.

I am not a statistician, but it is interesting to observe stochastic indicators that may be suggesting that markets have tested the same bottom on four occasions, in February of this year, and again in May, and again in July, and most recently, at the end of September. In and of itself, this is not an actionable piece of data, but when viewed holistically with other metrics, it looks characteristic of market behavior when trying to coalesce around a bottom.

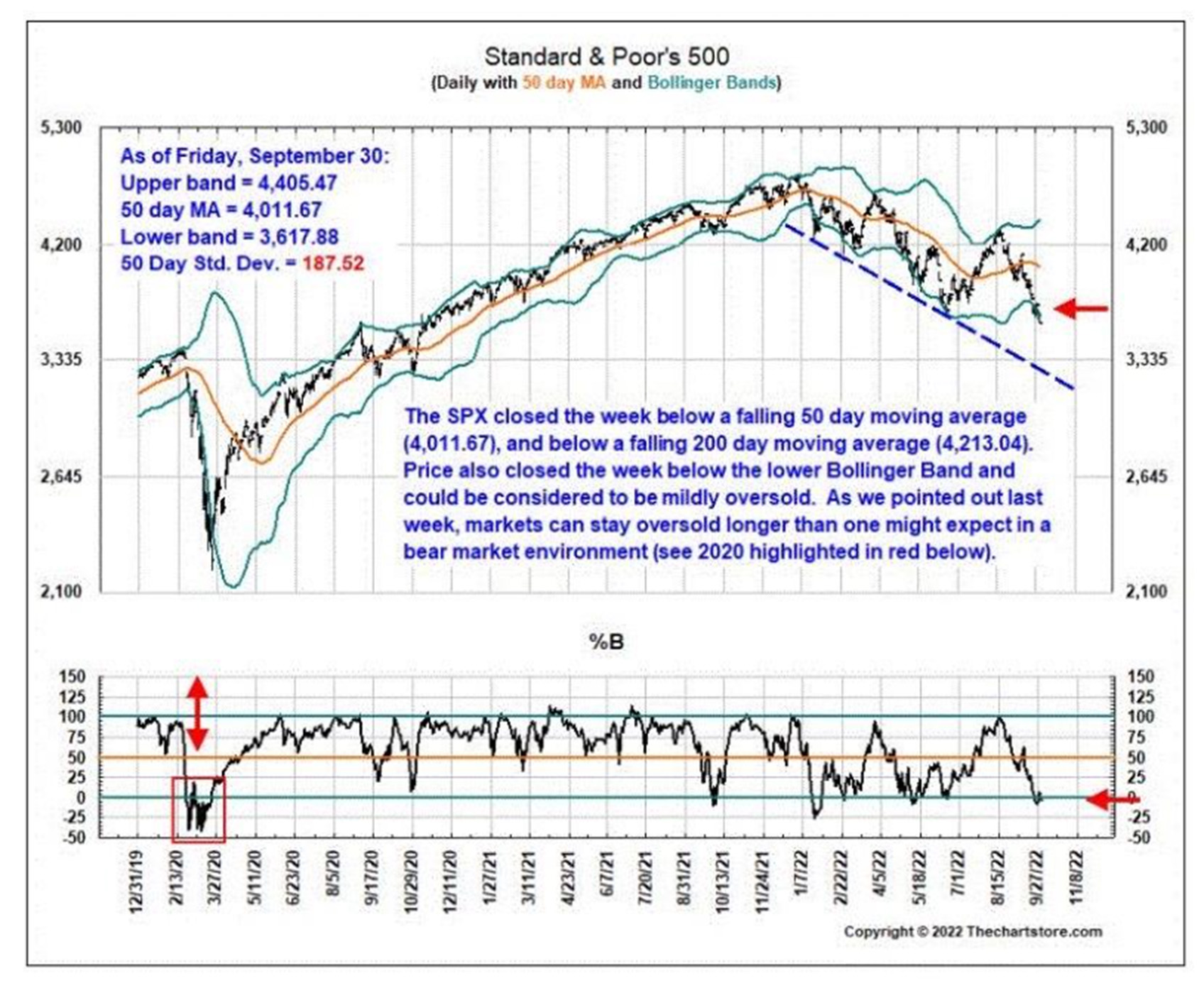

At the end of September, only 3% of the S&P 500 stocks were trading above their 50-day moving average. This is profound, because at the beginning of September, 92% of the stocks in the S&P 500 index were trading above their 50-day moving average.

While this was happening, we saw a significant increase in the ratio of open put to call interest. Normally, this is indicative of excessive fear and we can also cross check this by looking at the VIX index, which recently touched a 52-week high with a reading of 38.94. Mutual fund outflows also spiked in September. We see things like this when the average investor is wringing their hands, and saying “I’m emotionally exhausted”. Lock in the losses, and get me out.

While this was happening, we saw a significant increase in the ratio of open put to call interest. Normally, this is indicative of excessive fear and we can also cross check this by looking at the VIX index, which recently touched a 52-week high with a reading of 38.94. Mutual fund outflows also spiked in September. We see things like this when the average investor is wringing their hands, and saying “I’m emotionally exhausted”. Lock in the losses, and get me out.

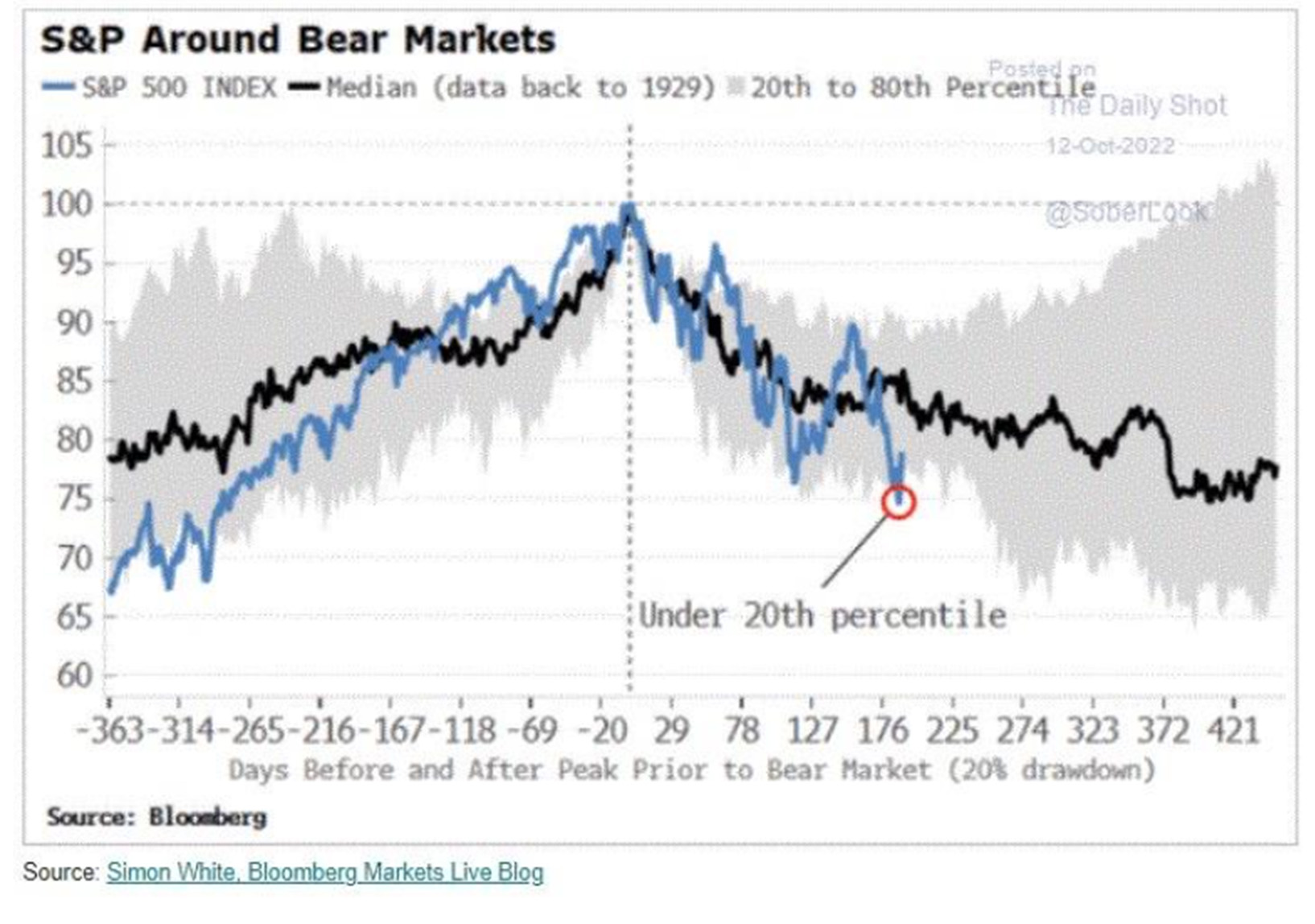

Let me wrap up this part of the commentary by drawing reference to this chart. It depicts all bear market cycles going back to 1929. The black line is the median result for all bear markets, and the blue line represents where we are now in this cycle. The shaded gray area represents the collage of all bear market cycles going back to 1929. Relatively, this chart suggests that we are below the median for all cycles, and also at the bottom of all such cycles, this many days into the event.

To me, this suggests that markets are overly sold, and probably because markets have priced into themselves more nefarious assumptions than what we might actually realize.

To me, this suggests that markets are overly sold, and probably because markets have priced into themselves more nefarious assumptions than what we might actually realize.

Within my article from last month, I drew reference to a chart, that depicts emotional states of being across the economic cycle. I suggested then that I thought we were drawing near to the capitulation phase, and thirty days later, I believe we have increasingly greater, quantifiable evidence that suggests this may be the case.

All of this is important, because if we are indeed coalescing around a bottom, and you’re not in the market, then in my opinion, you run an even greater risk that comes with talking yourself out of participating in the recovery when it occurs.

So in conclusion, regardless of the period of time, or the state of the economy, the achievement of long-term goals is predicate on the consistency with which you meet the implementation of the strategy. The composition of the investment accounts will change to reflect current periods of time, but the approach, dedication, and commitment to the strategy should be unwavering.

So in conclusion, regardless of the period of time, or the state of the economy, the achievement of long-term goals is predicate on the consistency with which you meet the implementation of the strategy. The composition of the investment accounts will change to reflect current periods of time, but the approach, dedication, and commitment to the strategy should be unwavering.

Even missing a few years, with the thought of letting a volatile period of time pass you by, can have a detrimental impact, 40 years down the road, on the potential success of long-term plans. I know that everyone is weary of this strange and unique year, but I believe that we’re drawing near to a point of inflection, and now is the time to have conviction, and intestinal fortitude, to work through periods of time such as this, and avoid the risk that comes with riding the emotional roller coaster.

(*) David R. Guttery, RFC, RFS, CAM, is a financial advisor, and has been in practice for 31 years, and is the President of Keystone Financial Group in Trussville. David offers products and services using the following business names: Keystone Financial Group – insurance and financial services | Ameritas Investment Company, LLC (AIC), Member FINRA / SIPC – securities and investments | Ameritas Advisory Services – investment advisory services. AIC and AAS are not affiliated with Keystone Financial Group. Information provided is gathered from sources believed to be reliable; however, we cannot guarantee their accuracy. This information should not be interpreted as a recommendation to buy or sell any security. Past performance is not an indicator of future results.

{kind=link}