By David R. Guttery, RFC, RFS, CAM

President, Keystone Financial Group-Trussville Al

Today, I’d like to discuss the impact of sentiment and states of mind, and how that must be appropriately managed when helping clients reach their planning goals.

Sentiment is real. It has a discernible impact on asset valuation, and we must be observant of that as we are navigating through challenging periods of time. I have encouraged my clients to remember that this is a marathon, not a sprint. In my opinion, this will not likely be one of those V-shaped patterns of economic recovery. Because of this, it is increasingly imperative to find intestinal fortitude, and to have patience as we attempt to separate fact from fiction, and navigate through palpable sentiment.

Sentiment is real. It has a discernible impact on asset valuation, and we must be observant of that as we are navigating through challenging periods of time. I have encouraged my clients to remember that this is a marathon, not a sprint. In my opinion, this will not likely be one of those V-shaped patterns of economic recovery. Because of this, it is increasingly imperative to find intestinal fortitude, and to have patience as we attempt to separate fact from fiction, and navigate through palpable sentiment.

Off-the-cuff, one observation that I can offer as it pertains to sentiment is that it will eventually dissipate. It will only dissipate however with time. Keep in mind that the magnitude of the event behind the sentiment is also important. Think of it this way. If you throw a small pebble in the water, it will form small rings that will dissipate quickly. However, if you throw a large boulder in the water, those waves will be larger and require more time to dissipate. We have experienced several pandemic related boulders over the last three years. So, expecting the resulting negative sentiment waves to dissipate quickly in a V-shaped manner is not reasonable.

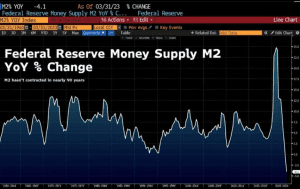

We’ve talked in the past about the unusual characteristics of this post crisis period of time. We’ve talked about the difficulty that comes with relying on anecdotal evidence when it is 90 years old.

In many ways, this is the most challenging time of my 33-year career, but it is at times such as these when it is necessary to be dispassionate, and with a thick skin, attempt to find the quantifiable singularity hidden behind the fog of sentiment. If it exists, then we take steps to avoid it. If it doesn’t exist, then you must attempt to make any market-based dislocations of value work in your favor.

In many ways, this is the most challenging time of my 33-year career, but it is at times such as these when it is necessary to be dispassionate, and with a thick skin, attempt to find the quantifiable singularity hidden behind the fog of sentiment. If it exists, then we take steps to avoid it. If it doesn’t exist, then you must attempt to make any market-based dislocations of value work in your favor.

I’d like to elaborate upon what I perceive to be the top areas of angst that have served to fixate market attention, and hopefully provide some perspective that may be of benefit at this time. As I’m discussing these, I would also like to offer my thoughts on the consumption of information, and how this can serve to amplify the impact of negative sentiment. Lastly, I will offer some thoughts on strategic action that can be taken to insulate your portfolio from the impact of overly negative sentiment.

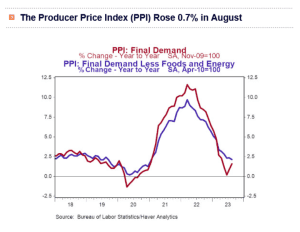

Let’s start with an observation about inflation. By the data, inflation has indeed abated sharply. In 14 of the previous 16 months, the consumer price index, the producer price index, and the PCE deflator have all declined. Indeed, the most recent data suggests that on average, wages rose by faster rate than did inflation. That’s quantifiable, factual, and a fantastic sign!

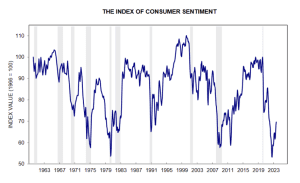

Unfortunately, if I were to ask the average person on the street if they believed that inflation was cooling, they would probably look at me as though I had a third eye. The truth is that inflation is indeed getting better. The perception however is that we remain under significant economic stress. This is a function of time. It’s the duration of the event, not where we are in the cycle.

Unfortunately, if I were to ask the average person on the street if they believed that inflation was cooling, they would probably look at me as though I had a third eye. The truth is that inflation is indeed getting better. The perception however is that we remain under significant economic stress. This is a function of time. It’s the duration of the event, not where we are in the cycle.

For nearly 2 years, the opposite was true, and inflation was significantly higher than the rate by which our incomes were increasing. In my opinion, people largely still feel poor, and this has impacted consumer sentiment. If you don’t have an optimistic outlook as a consumer, then generally patterns of consumption will reflect that negativity. It has just gone on for so long.

There is a negative feedback loop at work here. For nearly 2 years, our ability to consume has gone backwards. Recent research shows that nearly two thirds of American households remain living paycheck to paycheck.

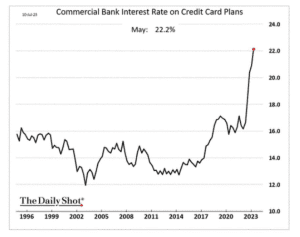

According to the Federal Reserve, nominal credit card debt is at an all-time high. Due to the removal of accommodation, bond yields have risen sharply, taking interest rates with them. According to Dave Haviland, average credit card interest rates are at a multi-decade high.

If gross domestic product is 70% consumption, and our ability to consume has declined over the last two years, while we are amassing a record amount of credit card debt, that is now very expensive to service, then one data point is not going to reverse this trend and create a positive feedback loop. It will take time. We need to have an extended period of time where inflation is muted, wages are increasing, and our ability to consume is consistently expanding, before we can expect attitudes toward consumption to change, and therefore patterns of consumption to change.

If gross domestic product is 70% consumption, and our ability to consume has declined over the last two years, while we are amassing a record amount of credit card debt, that is now very expensive to service, then one data point is not going to reverse this trend and create a positive feedback loop. It will take time. We need to have an extended period of time where inflation is muted, wages are increasing, and our ability to consume is consistently expanding, before we can expect attitudes toward consumption to change, and therefore patterns of consumption to change.

Metaphorically, in my opinion, this will be akin to watching grass grow. It will be slow, and arduous. Again, this will likely be an economic marathon, requiring much patience as we endure the sentiment that remains following an extended period of inflation induced stress on the consumer.

There are other areas of concern that remain with the full attention of market participants. First, there is a concern that the Federal Reserve will revert to an overly draconian stance as it continues to remove accommodation. Indeed, in my opinion the truth is that the Federal Reserve has not deviated from their approach since March of last year.

Did the Fed shock the markets? Yes. As we’ve discussed in the past, I believe that market participants conflated the removal of accommodation, with the fighting of inflation. Indeed, these are two discernible, and mutually exclusive objectives. Between the Federal Reserve, and the expectations of market participants, I believe the Federal Reserve has been consistent, while the market continues to incorrectly out guess the Federal Reserve. In my opinion, fear over an overly restrictive Federal Reserve is not grounded in factual observation.

Did the Fed shock the markets? Yes. As we’ve discussed in the past, I believe that market participants conflated the removal of accommodation, with the fighting of inflation. Indeed, these are two discernible, and mutually exclusive objectives. Between the Federal Reserve, and the expectations of market participants, I believe the Federal Reserve has been consistent, while the market continues to incorrectly out guess the Federal Reserve. In my opinion, fear over an overly restrictive Federal Reserve is not grounded in factual observation.

We have talked throughout the year about the potential for recession. Indeed, I’m hearing opinions in the media that another 2008 style recession event may be on our doorstep.

However, I am also hearing many economists describing this in terms of being a rolling recession. Well, at heart I am an optimist. A rolling recession implies that you are also in a rolling recovery. It is the word rolling however that jumps off the page in my opinion. We have seen double dip recessions, but never a rolling recession.

That implies long-term. For well over a year, I have suggested that I thought we would find ourselves in such an economic event. Again, this being a marathon, it will take time for the current negative feedback loop to reverse course. That will not happen overnight. Therefore, in my opinion, I believe that what we are seeing now, and what we will likely see over the next few years, is an economy that struggles to find traction. Market participants however believe, in my opinion, that a long and deep recession remains in our future. To this point anyway, I fail to see any quantifiable evidence behind that fear.

That implies long-term. For well over a year, I have suggested that I thought we would find ourselves in such an economic event. Again, this being a marathon, it will take time for the current negative feedback loop to reverse course. That will not happen overnight. Therefore, in my opinion, I believe that what we are seeing now, and what we will likely see over the next few years, is an economy that struggles to find traction. Market participants however believe, in my opinion, that a long and deep recession remains in our future. To this point anyway, I fail to see any quantifiable evidence behind that fear.

Earlier in the year there was concern that the United States would default on its debt. In the history of the United States, that has never happened, but that did not stop the market from worrying about it over the summer as budget negotiations in Washington stalled.

Currently, we are hearing about the United Auto Workers strike, and how that could serve to exacerbate an anticipated deep and long recession.

The war between Russia and Ukraine continue to amplify geopolitical concerns. Over the weekend, war erupted in Israel. We have an election cycle on the horizon. The market is replete with shiny objects that are captivating the attention of market participants. The more fixated attention becomes on these areas, the more shortsighted market participants can become. In an environment like this, overly negative sentiment can run rampantly. I believe this is where we are, and now the larger question is how do we manage the sentiment while we are pursuing planning objectives.

The war between Russia and Ukraine continue to amplify geopolitical concerns. Over the weekend, war erupted in Israel. We have an election cycle on the horizon. The market is replete with shiny objects that are captivating the attention of market participants. The more fixated attention becomes on these areas, the more shortsighted market participants can become. In an environment like this, overly negative sentiment can run rampantly. I believe this is where we are, and now the larger question is how do we manage the sentiment while we are pursuing planning objectives.

One piece of advice that I routinely convey to clients is to be mindful of your exposure to information. Today, we are bombarded with information over our mobile phones, our computers, the television, and the internet. This can serve as a breeding ground for misinformation, and disinformation, and sometimes it can be easy to accept such at face value without digging below the surface to verify the validity of articles and opinions. I encourage my clients to give a very wide birth to sensationalism. Avoid it. Behind my side of the desk, I spend my time following a rules-based approach, following dispassionate and quantifiable data.

In my opinion, this data does not seem to justify much of the negative sentiment that seems to be hanging over the market, and therefore, I believe there are many opportunities for those with the intestinal fortitude to remain vigilant. In previous videos, we have referred to these as being coiled springs. As negative sentiment and market angst serve to crimp a spring into a tight coil, potential energy grows. That energy will not be released however, and converted to kinetic energy until a catalyst is present. What might that catalyst be? Could it be an unexpectedly positive remark from an analyst? Could it be a significantly better quarterly report on earnings and revenue? The paradox of a coiled spring is that you must be sitting on it before it pops if it is to be of any benefit in your portfolio.

You’ve heard this before, and it is not a cliché. Be greedy when others are fearful. In my opinion, there is a lot of fear in the market now, that in my opinion cannot be validated with quantifiable data. At times such as these, for those with a thick skin, and cast-iron fortitude, it would be of benefit to remain dispassionate, and let the data be your guide. Much like a pilot relies on instrumentation when visibility is opaque, if we are going to fly through this fog of negative sentiment, we must rely on that which we can quantify.

Just remember this is a marathon. This will not be over tomorrow, and patients is worth its weight in platinum. I would suggest that everyone take several steps back from the trees, to observe the forest. Remain focused on the objectives that you have codified in your long-term planning. At the end of the day, what happens in the market in the short term is not as important as making progress toward the achievement of these goals. Yes, we may have endured some unusually difficult post-pandemic years, but since the inception of your plan, on average per year, are you still ahead of the targets outlined within your plan? If so, then you’re still on pace to achieve those goals. Day to day, exposure to risk should be tactical, and driven by a rules-based, economically data-driven approach. Long-term however, we can lose sight of the objectives were trying to achieve if we are focused on the latest sensationalism of the day. Take a step back, evaluate where you are, and breathe.

(*) David R. Guttery, RFC, RFS, CAM, is a financial advisor, and has been in practice for 32 years, and is the President of Keystone Financial Group in Trussville. David offers products and services using the following business names: Keystone Financial Group – insurance and financial services | Ameritas Investment Company, LLC (AIC), Member FINRA / SIPC – securities and investments | Ameritas Advisory Services – investment advisory services. AIC and AAS are not affiliated with Keystone Financial Group. Information provided is gathered from sources believed to be reliable; however, we cannot guarantee their accuracy. This information should not be interpreted as a recommendation to buy or sell any security. Past performance is not an indicator of future results. Examples are for illustrative purposes only and should not be considered representative of any investment. Investments involve risks, including loss of principal.

{kind=link}